1/16 – 1/19 Biotech Moonshots Update

1/16 – 1/19 Biotech Moonshots Update

Profiting From $20-for-$1 Biotechs

The biotech bear market from February 2021 through October 2023 created some dramatically underpriced stocks. There is free money lying on the sidewalk, just waiting for you to pick it up.

Dear Biotechies:

So December retail sales were up 0.6% and that was enough for the market to fear the bogeyman...err, Chairman Powell...might not cut rates as soon as they thought. So down went stocks Wednesday. Well, duh.

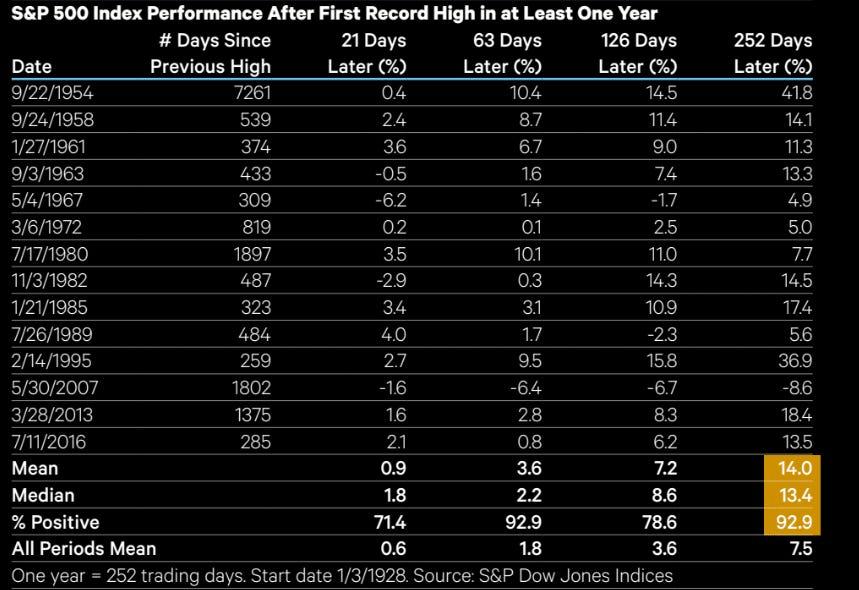

Today's record S&P 500 close should get some of the sideline money throwing in the towel and buying stocks. What happens after an all-time high? The S&P 500 has outperformed its long-term average one-, three-, six-, and 12-months later. The one-month returns are not quite as strong, suggesting a short-term overbought condition in some cases. One year later, the S&P 500 has risen 13 out of 14 times by a median of 13.4%. The S&P 500 and Dow Jones Industrials set all-time highs today, and the Nasdaq Composite set a 52-week high, supporting the case for further gains.

h/t The Market Ear

It's important for you to know that my economic outlook for 2024 is pretty different from Wall Street. A recent BofA poll showed US stock optimism at the highest level since 2021. BofA said there is “record optimism on rate cuts” and 79% of survey respondents expect the global economy to experience either a soft or no landing in 2024. Most respondents saw stocks as the best way to play the Fed rate cutting cycle.

Wall Street: The Fed will start cutting rates as early as March, surely by May; there will be no negative quarters for real GDP; the S&P 500 will touch 5000.

Me: The Fed will NOT cut rates until the Fall, if then (High for Longer); there will be two negative quarters of real GDP; but the S&P 500 will touch 5000 anyway

If I'm right, this will be the usual fourth year of a Presidential term with high-level churning that frustrates both bulls and bears, reduces the profit potential of buying options, and is a stockpicker's market that provides regular buying opportunities and rewards fundamental progress.

At the same time, more market gurus are coming around to my position that we are in a secular bull market that will continue for many years. We could see the S&P 500 top at 15,000 in 2036. I disagree on some of the details in the BofA chart below (if you were investing in 1981 and 1982, you wouldn't say a bull market started in 1980), but it is broadly correct.

h/t @AdamCorleoneJr

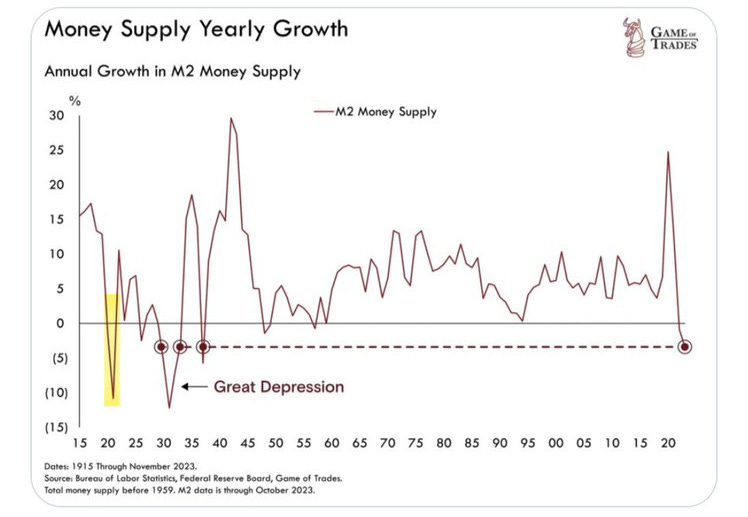

One big reason we are headed for a shallow recession is the M2 money supply is contracting for the first time since the 1930s.

h/t @GameofTrades_

The Fed's favorite mouthpiece, @NickTimiraos of The Wall Street Journal, said the speed with which balances in the Fed’s overnight reverse repurchase agreement (ONRRP) facility have fallen over the last few months and the faster rate of Treasury balance sheet runoff are prompting Fed officials to start thinking about slowing down (but not ending) QT for Treasuries. That's one reason the recession will be shallow, not deep.

A second reason is a large swath of the economy has become less sensitive to rising interest rates because so many borrowers, both homeowners and corporations, refinanced their debt at low rates in 2020 and 2021.

A third reason is the extremely high labor demand after the Covid lockdowns ended seems to have been largely worked off, per the JOLTS (Job Openings and Labor Turnover Survey) data. The starting point for this labor market cycle was so high that a 2.4 percentage point drawdown in labor demand has so far only led to a slowdown. Normally we would be in a recession already with these numbers. (h/t @stifelinst).

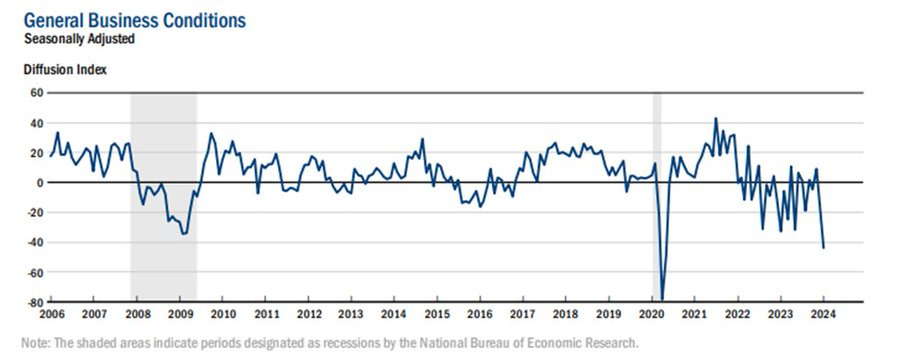

A fourth reason is that the manufacturing sector has been in a recession for months. The Institute for Supply Management (ISM) purchasing manager’s survey (PMI) peaked in March 2021 and has been below 50 (contraction) since October 2022. The Empire State Fed January survey crumbled to its second lowest level ever (May 2020, during Covid, was the worst) driven by sharp declines in new orders and shipments.

h/t @cvpayne

The yield curve just “de-inverted” as the yield on 2-year Treasury notes finally went below the yield on the 30-year bond for the first time since July 2022. Some on Wall Street think that means a recession is called off. Not so fast.

In the 2008 cycle, manufacturing production didn't turn down until 16 months after the yield curve inverted in December 2007. Recession fatigue is at an extreme today only about 13 months after the 10-year/3-month inversion set off warning bells. It's been quickly forgotten how long the 2008 cycle took.

Market Outlook

Through yesterday, the S&P 500 was flat since last Thursday and remains stuck inside the 4720 to 4840 range. Chasing breakout moves in either direction has been a costly mistake so far. The Index is clinging to a 0.2% gain year-to-date. The Nasdaq Composite did a little better, gaining 0.5%. It now is up 0.3% for the year. The small-cap Russell 2000 dropped 1.6% as relative weakness continued in small-caps. It is down 5.1% in 2024.

There are about two weeks left of the buyback blackout window. Companies will start to exit blackout as they report earnings and then can start buying their stock again.

h/t The Market Ear

The fractal dimension is still in an uptrend that has taken us to a new all-time high – but probably not much further.

Economy

The Atlanta Fed's GDPNow model forecast for December quarter GDP increased to 2.4% due to increases in personal consumption expenditures growth and private domestic investment growth. The first official number comes next Thursday morning.

What the presumed soft landing looks like, per BofA:

h/t @dailychartbook

Let's focus in on their 2024 Gross Domestic Product forecasts. I think we'll see at least two quarters with minus signs. They don't. But it could be called a soft landing and a Fed success either way.

Biotech

Biotech stock price performance has a strong seasonality component that seems to be driven by the timing of major medical society annual meetings and the big brokerage firm conferences. Companies sometimes spend months analyzing interim clinical trial data and developing significant presentations for these events. When they announce breakthrough new results, partnerships, or other critical news, their stocks go up.

IBB tracks the ICE Biotechnology Index and XBI tracks the S&P Biotechnology Select Index. The graphic below shows the average performance of the XBI by month (left side) and the percentage of times each month is profitable (right side).

As you can see, January is a decent month with the big JPMorgan Healthcare Conference anchoring Biotech Week in San Francisco. February, not so much. Then returns improve through and just after the American Society of Clinical Oncology annual meeting (ASCO) in June. August is the worst month for biotech stocks both in Average returns and % positive, and September and October are not much better. After mutual fund window dressing sales end on October 31, the stocks get back in gear for the American Society of Hematology annual meeting (ASH) in December, followed by Biotech Week just after New Years.

The chart below from SentimenTrader displays the different annual seasonal trend for the iShares Biotechnology ETF (IBB). A favorable portion of the year begins at the close of Trading Day of Year (TDY) #87 and extends through TDY #179. For 2024 this period extends from the close on May 6 through September 16.

The chart below displays the hypothetical cumulative % return from holding biotech only during the seasonally favorable period, each year since 1986 through 2022.

And this is the performance of biotech stocks for all trading days NOT between #88 and #179.

The difference in performance is very dramatic if you overlay both charts into one graph.

The favorable period (TDY #88 through TDY #179) gained 2,075%. The rest of the year (TDY #1 through #87 and #180 through the end of the year) gained 168%.

Coming Events

All times below are ET, and most presentations and slides are archived on the companies' websites so you can listen to them.

Wednesday, January 24

Short Interest - After the close

Thursday, January 25

December quarter GDP - 8:30am – First estimate

Friday, January 26

Personal Consumption Expenditures Index - 8:30am

Biotech Moonshots Portfolio Update

This was a tough week for biotech stocks as the weak seasonality hit early. The Moonshots portfolio fell 5.3%, but there's enough clinical and other data coming to drive our performance much higher in 2024. Let's dig in…

* * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * *

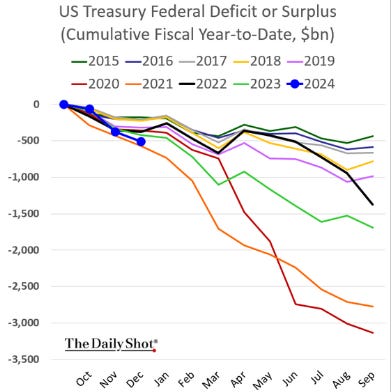

Pretty incredible to see Covid-like deficits being run at a time when unemployment is at secular lows and the economy is growing above potential. In the short-term this helps delay any recession incoming. Long-term it will make managing an eventual recession difficult.

h/t @BobEUnlimited

* * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * *

Your checking the REAL banned book list Editor,

Paid subscriber or not, if you would click the ♥ symbol below it would really help me get the word out.